How I’m Getting Back on Track With Investing This Year

I’ve been investing for a long time, and I usually talk a lot about consistency, compound interest, and building wealth over time. But here’s the honest truth…

I haven’t been investing consistently for the past two years.

Yes, I said it.

I’m not proud of it, but I’m also not ashamed to admit that life happened. The economy and inflation have been scary and caused many of us to want to hold on more to any cash we have while we brace for the impact of whatever is coming next. Then, my family had a few major financial goals that forced us to put investing on the back burner.

So investing dropped lower on the priority list.

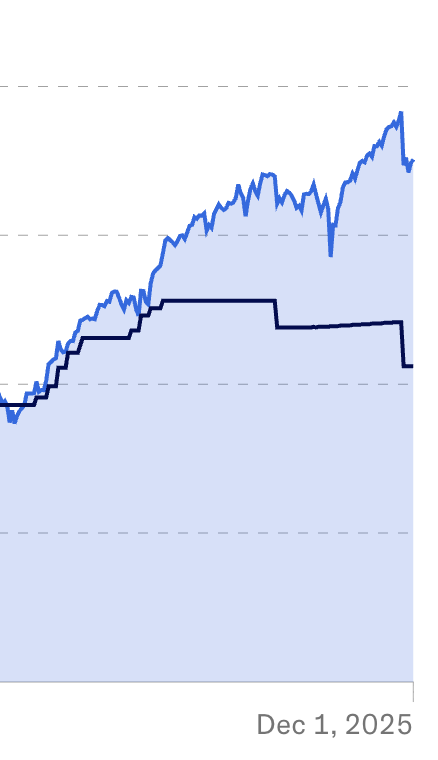

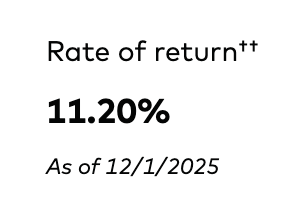

But here’s the twist: even though I wasn’t investing regularly, my portfolio still grew…significantly.

(My IRA)

(Brokerage Account)

So passively, in fact, that it completely reignited my motivation to get back on track.

And now, with our finances leveling out again, I’m putting investing back at the top of my priority list this year and in the years to come.

Check out how to Reset your Finances here

Here’s why, and exactly how I’m doing it.

Why I’m Getting Back Into Investing

1. What I do today will pay off tenfold tomorrow

Even without steady contributions, I watched both my IRA and my brokerage account grow thanks to compound interest and the market recovering. Seeing real growth I didn’t “work” for reminded me why investing matters.

This is what people mean when they say your money should work for you.

Watching those numbers rise made me realize just how powerful long-term investing really is.

2. The market always trends upward over time

Not every day. Not every month. Not even every year. But over the long haul? The stock market has historically risen.

I shared the price of Amazon stock on this blog about two years ago. Back then, it was $139.95 per share. Today, it’s $234.42 per share. That’s nearly a $100 increase, just for holding onto a solid investment. Moments like this remind me that delaying investing out of fear or uncertainty usually hurts more than it helps.

Of course investing comes with some risks. For example, Target’s stock has dropped in recent years, but that’s why it’s important to diversify your investments.

I use a robo-advisor called Betterment which invests in different stocks and bonds for me so I don’t have to worry about picking things out on my own. Betterment listens to your goals and preferences, then prepares a custom portfolio for you and balances it all on your behalf. I just pay a super small fee each year but it’s well worth it to just sit back and let Betterment do all the work while I focus on saving.

3. Wealth builds options, freedom, and flexibility

Money isn’t everything, but it does give you choices: where you live, how you work, what opportunities you take, and how you support your family.

When I wasn’t investing consistently, I felt that loss of momentum. It didn’t feel great. And now that we’re more settled financially, it’s time to rebuild that momentum with intention.

Check out how to Reset Your Finances here

How I’m Getting Back on Track

1. Resetting my mindset

Everything starts with mindset. If you don’t believe your goals are possible, or if you’re discouraged, it’s hard to take action.

Yes, things cost more than they ever have. Yes, money feels tighter. But I still believe I can save and invest. That belief fuels action.

2. Revisiting my budget

We’re already pretty frugal, but I’m revisiting our budget line-by-line. It’s not about cutting everything; it’s about making room for investing again.

Even a small amount has a big impact when you’re consistent.

Related: 5 Tips to Help You Save on a Low Income

3. Paying myself first (non-negotiable this time)

One of my major goals next year is to max out my IRA, which will have a limit of $7,500.

That comes out to $625 per month.

It sounds like a lot, but breaking it down monthly makes it feel manageable, and it forces me to prioritize long-term stability over short-term conveniences.

4. Limiting debt and avoiding new obligations

I do have a car loan, but my husband’s car is paid off, which helps a ton. We also don’t plan on taking on new debt anytime soon.

And honestly? We’re likely going to take a break from using credit cards for a bit. I don’t want the temptation to overspend or justify lifestyle creep.

Related: Have Debt But Want to Invest? Here’s What You Need to Know

5. Increasing my income (and being strategic about it)

Right now, I run this blog, freelance, and work part-time at a local store. I’ve been doing that part-time job for a year, but I’ll likely leave it sometime this year.

Before I let it go, I want to maximize that extra income. I’m also considering picking up a few mystery shopping gigs for “fun money” so I can funnel everything from blogging and freelancing toward:

- savings

- investing

- and essential expenses

Additional income gives me more fuel to reach my goals faster.

Check out how to Reset Your Finances here

6. Using Betterment for Hands-Off IRA Investing

I’ve had my IRA with Betterment for years, and I still love it.

Why?

Because it’s perfect for someone who wants to invest without needing to constantly research, rebalance, or guess. Betterment automatically:

- diversifies your portfolio

- rebalances it

- reinvests dividends

- and helps keep you aligned with your long-term goals

It’s truly “set it and forget it,” which is exactly what helped my account grow, even when I wasn’t contributing.

For my IRA, I’ll continue using Betterment because it keeps everything simple, low-maintenance, and automated.

7. Using Acorns for Micro-Investing (Spare Change Adds Up!)

This year, I’m also bringing Acorns back into the mix.

I love Acorns because it removes the pressure of “finding” money to invest. It does the work for you by rounding up spare change from everyday purchases and investing it automatically.

Saving $0.12 here and $0.41 there may not seem like much, but it builds up. Saving something is better than saving nothing.

I plan to let Acorns run quietly in the background while I focus on my larger investing goals.

8. Rebuilding my consistency systems

It’s easy to start investing. The challenge is staying consistent.

This year, I’m:

- automating contributions

- scheduling a monthly “money date” with my husband

- setting micro-goals (like $50–$100 extra per week)

- tracking my net worth again

- and keeping investing at the top of my budget

Every little habit I rebuild helps strengthen the bigger picture.

Let’s Get Back on Track Together

Final Thoughts

Taking two years off from investing wasn’t ideal, but it was real because life happens. But what surprised me most was that my portfolio kept growing, even during the pause.

That growth reminded me of one simple truth: It’s never too late to begin again.

This year, I’m stepping back into investing with more clarity, more stability, and more motivation than ever before.

Investing doesn’t have to be a distant goal for you either. You can start preparing your mindset and your finances right now. If you’re looking for more financial stability, clarity, and confidence, I highly recommend joining my program, Reset Your Finances.

It’s a practical, step-by-step system to help you organize your money, create better habits, and build a financial foundation that supports big goals, like investing, saving, and paying off debt. You can learn more about getting started here.

If money feels messy, confusing, or overwhelming right now, you don’t need more information; you need a reset. Reset Your Finances helps you get clarity, build confidence, and take control of your money one step at a time.

Click here to learn more about Reset Your Finances and move forward with confidence.